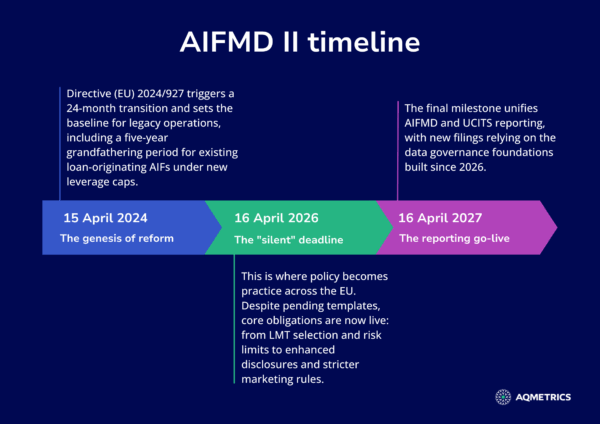

The arrival of the 16th April 2026 marks the most significant evolution of the European alternative investment landscape since the original directive’s inception in 2011. For many Alternative Investment Fund Managers (AIFMs), a tempting narrative has begun to circulate: that because the new Annex IV reporting templates aren’t due for submission until 2027, the pressure is off for another twelve months.

This is a misconception that could prove fatal to a firm’s compliance standing and institutional reputation. While the formal XML filings under the new Regulatory Technical Standards (RTS) are indeed deferred to the 16th April 2027, the legal obligation to comply with the substantive requirements of Directive (EU) 2024/927 (AIFMD II) begins as of the April 2026 deadline.

For the modern AIFM, the “silent deadline” of 2026 is where the real work happens. Trust is built on data lineage, and the data gathering required for your first 2027 report starts this April. This post explores why the transition from AIFMD I to AIFMD II is an operational transformation rather than a mere filing update.

The 2027 paradox: you cannot report what you haven’t tracked

The industry is currently navigating a “reporting paradox”. On 16th April 2027, every authorised AIFM will be required to submit a highly granular report to their National Competent Authority (NCA) that reflects their operations during the 2026–2027 transition year. Unlike previous updates, AIFMD II introduces metrics that are inherently longitudinal: they cannot be reconstructed through a retrospective year-end audit.

If your internal data architecture is not capturing these metrics as of April 2026, your 2027 filing will contain “data holes” that signal a failure of governance to your regulator. Specifically, the directive mandates the reporting of all relevant instruments, exposures, and markets, removing the previous discretion to report only “principal” holdings.

The shift in asset identification

Under AIFMD I, managers often had leeway in how they tagged and categorised assets. AIFMD II enforces a harmonised EU format that relies on standardised identifiers to link reported data to public and supervisory sources. This requires:

- Standardised identifiers: integration of Legal Entity Identifiers (LEIs), International Securities Identification Numbers (ISINs) and Market Identifier Codes (MICs) for every single portfolio position, regardless of its size or liquidity.

- Data enrichment: mapping hundreds of internal data points to approximately 340 distinct fields in the new Annex IV template.

- Real-time tracking: because the 2027 report must reflect the state of the fund throughout the preceding year, the “tagging” must be accurate from the moment of trade execution.

Regulatory convergence: the rise of UCITS VI

The implementation of AIFMD II does not exist in isolation; it represents a broader push toward regulatory convergence through the parallel update of the UCITS framework, frequently referred to as UCITS VI. Both regimes are now legally intertwined, sharing a transposition deadline of 16th April 16 2026, and aiming to eliminate regulatory arbitrage between alternative and retail fund structures.

This alignment is most visible in three key areas:

- Liquidity management harmonisation: UCITS managers must now follow the same mandate as AIFMs to select at least two LMTs from the harmonised EU list and implement detailed activation policies.

- Supervisory reporting mirroring: UCITS VI introduces a formal supervisory reporting regime for management companies that closely mirrors the logic and structure of AIFMD Annex IV. For the first time, UCITS managers will need to regularly report granular data on traded instruments, markets, exposures and the results of liquidity stress tests.

- Delegation oversight: tighter rules on delegation and substance now apply across both regimes, requiring management companies to demonstrate that delegates are selected with due care and monitored via standardised FTE and resource metrics.

By synchronising these requirements, the European Union is moving toward a single, robust standard for European fund governance, regardless of whether the vehicle is aimed at retail or institutional investors.

Substance and the human capital metric: the FTE challenge

Perhaps the most significant change in reporting philosophy is the requirement to report human resources in a structured, quantitative format. AIFMD II moves beyond the narrative “program of activity” to require hard numbers on the AIFM’s internal substance.

The two-person rule and FTE counts

AIFMD II codifies the requirement for at least two natural persons to conduct the business of the AIFM. These individuals must be domiciled in the EU and employed full-time (or committed full-time as executive members).

However, the reporting requirements go much deeper. Starting on 16th April 2026, AIFMs must track:

- Portfolio/Risk Management FTEs: the number of Full-Time Equivalents (FTEs) performing day-to-day portfolio and risk management tasks internally within the AIFM.

- Delegation Monitoring FTEs: the specific number of FTEs dedicated solely to the monitoring of delegated activities.

This requires a sophisticated methodology for time-allocation. It is no longer sufficient to state that a senior manager “oversees” a delegate; the firm must be able to quantify the human resources committed to that oversight. Managers who fail to implement internal resource-tracking today will find it impossible to populate these fields accurately in twelve months.

Delegation oversight: from “box-ticking” to “active audit”

The European Securities and Markets Authority (ESMA) has historically viewed delegation as a risk-oversight challenge. AIFMD II does not prohibit delegation, recognising its role in accessing specialised expertise, but it significantly raises the burden of proof for the AIFM’s accountability.

The audit trail of oversight

Under the new regime, regular regulatory reporting must include:

- Due diligence cycles: the exact dates and outcomes of periodic due diligence reviews performed on each delegate.

- Issue identification: a list of any issues identified during these reviews.

- Remediation timelines: a clear record of the measures adopted to address those issues and the specific dates by which they were implemented.

By requiring this level of granularity, AIFMD II effectively mandates that the AIFM acts as an “active supervisor” of its own delegates. This shift is intended to prevent the creation of “letter-box entities” and to ensure that the AIFM remains the seat of control, regardless of where the underlying portfolio management occurs .

Liquidity management: from toolbox to mandatory framework

For open-ended funds, the 16th April 2026 marks the end of the “voluntary” approach to liquidity management. Influenced by the market volatility of recent years, ESMA has mandated a harmonised framework for Liquidity Management Tools (LMTs).

The selection mandate

Managers of open-ended AIFs must select at least two appropriate LMTs from a prescribed list in Annex V (or one for money market funds). These tools must be:

- Strategy-aligned: appropriately matched to the fund’s investment strategy, liquidity profile and redemption frequency.

- Constitutional: integrated into the fund’s constitutive documents (e.g. the Limited Partnership Agreement or Articles of Association).

- Procedural: supported by detailed internal policies governing their activation, deactivation and calibration.

ESMA distinguishes between “quantitative” tools (like redemption gates or notice extensions) and “anti-dilution” tools (like swing pricing or anti-dilution levies). While not a strict legal requirement, the regulator strongly recommends a “balanced” approach, selecting one tool of each type to manage both volume-based stress and cost-based dilution.

Notification protocols

The 2026 deadline is not just about selection; it is about communication. AIFMs must notify their NCA of the selected tools and provide the corresponding policies. In Luxembourg, for instance, the CSSF has already launched dedicated modules for “LMT Selection” and “LMT activation” to facilitate this real-time reporting.

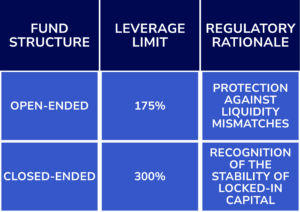

Private credit and the LO-AIF standard

AIFMD II introduces the first harmonised European framework for the rapidly expanding private credit sector. The directive creates a new fund category: the “Loan-Originating AIF” (LO-AIF), defined as any fund whose principal strategy is to originate loans or where originated loans account for at least 50% of the NAV.

Hard leverage caps

To mitigate systemic risk, LO-AIFs are now subject to strict leverage caps, calculated using the commitment method:

Leverage Ratio = Total Exposure (Commitment Method) / Net Asset Value

Risk retention and borrower limits

The directive effectively prohibits “originate-to-distribute” strategies by requiring the AIF to retain an economic interest of at least 5% of the notional value of any loan it originates and subsequently transfers. Furthermore, to prevent excessive concentration, an LO-AIF cannot originate loans to a single borrower (if that borrower is a financial undertaking, AIF or UCITS) exceeding 20% of the fund’s capital.

These rules apply to any new loan originated after 16th April 2026, even for funds that benefit from transitional grandfathering periods for their overall leverage levels.

Investor trust through Article 23 Disclosures

Transparency is the bedrock of investor trust and AIFMD II significantly raises the bar for pre-contractual and periodic disclosures. Under the updated Article 23, the era of disclosing “maximum annual fees” is over.

Comprehensive fee itemisation

AIFMs are now mandated to provide a comprehensive list of all fees, charges and expenses borne by the manager in connection with the operation of the AIF and that are directly or indirectly allocated to the fund. This includes:

- Administrative costs: origination fees, servicing fees, and legal/compliance costs.

- Ancillary charges: any costs related to the administration of loans for debt funds.

- Annual reporting: an annual update to investors on all fees actually borne by them during the year.

By providing this level of clarity, expert-led firms can demonstrate institutional maturity, signalling to allocators that their governance framework is robust and their cost structures are defensible.

The global dimension: accessing the EU via NPPR

For non-EU managers (such as those in the US or UK) utilising the National Private Placement Regime (NPPR) under Article 42, AIFMD II introduces new “conditions of entry” that mirror internal standards.

The AML and tax jurisdictional hurdles

Marketing within the EU is now strictly contingent on the fund’s domicile and the manager’s home jurisdiction not appearing on:

- The EU high-risk third country list: replacing the previous FATF “non-cooperative” standard.

- The EU list of non-cooperative tax jurisdictions: funds domiciled in “blacklisted” jurisdictions like Panama or Vanuatu are immediately barred from EU marketing.

Furthermore, the manager must ensure that a tax exchange agreement (compliant with OECD standards) exists with every single Member State where marketing is taking place. These are immediate requirements; there is no grace period for funds currently in the market.

Strategic opportunity: ancillary services

While much of AIFMD II focuses on increased oversight, the directive also broadens the scope of permitted activities an AIFM can conduct. Authorised firms can now expand their business models into:

- Benchmark administration: pursuant to the Benchmarks Regulation.

- Credit servicing: under the Credit Services Directive.

- Third-party services: providing the same operational or risk-management functions (like IT or HR services) to third parties that they already perform for their own funds.

This allows specialised firms to monetise their regulatory infrastructure, evolving from simple fund managers into comprehensive asset-servicing platforms.

Conclusion: the gathering starts today

The successful implementation of AIFMD II is a two-stage process: a legal and operational transformation in 2026, followed by a technical reporting debut in 2027.

The 2026 transposition date is the true deadline for change. AIFMs that treat the 2027 template update as their starting point will discover, too late, that the data they are required to report (of human resource allocations, of due diligence outcomes, of granular asset identifiers) has already been lost to time.

16th April 2026 is the day the industry proves it has the governance, the systems and the data integrity to operate in a harmonised European market. The gathering starts now.

Strategic checklist for the 2026 silent deadline

- Data architecture: audit systems to ensure ISIN, LEI and MIC identifiers are integrated for 100% of portfolio assets.

- Human capital: implement time-tracking methodologies to support FTE reporting for internal management and delegate oversight.

- Liquidity management: board-level approval of at least two LMTs for every open-ended AIF, supported by a formal policy communicated to the NCA.

- Private credit frameworks: for LO-AIFs, implement real-time monitoring of leverage against 175%/300% caps and maintain the 5% risk retention record.

- Investor disclosure: refresh Article 23 disclosures to move from “maximum fee” to a comprehensive itemised list of all direct/indirect charges.

- Third-country compliance: verify that fund domiciles are not on the EU’s AML or non-cooperative tax lists before commencing any new marketing activity.

- Map UCITS reporting capabilities to align with the new Annex IV-style mandates.

Turn DORA into a digital credential

Our platform is engineered to move you past the paper-based compliance of 2025 and into the high-governance, data-driven reality of 2026. AQMetrics provides a “single regulatory source of truth” for DORA, eliminating the “data-reload loop” that causes most firms to miss deadlines. Don’t let DORA become a liability. Transform it into a digital credential that signals resilience and reliability to your investors and regulators.